Setting up a Limited Liability Partnership in the UK can feel overwhelming for small business owners navigating complex legal requirements and statutory filings. Many entrepreneurs struggle with understanding what documents they need, how to register properly, and what compliance obligations they must meet to avoid penalties. This guide breaks down the LLP formation process into clear, manageable steps, covering everything from initial preparation and partner registration to ongoing compliance in 2026. You will learn exactly what prerequisites you need, how to file your incorporation documents correctly, and how to maintain your LLP legally.

Table of Contents

- Understanding An LLP And Its Benefits

- Preparing To Set Up Your LLP: Legal Requirements And Documentation

- Steps To Form And Register Your LLP In The UK

- Ensuring Ongoing Compliance And Managing Your LLP Effectively

- Enhance Your LLP Setup With Expert Resources

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Hybrid structure | LLPs combine partnership flexibility with limited liability, protecting partners’ personal assets from business debts. |

| Formal agreement required | A comprehensive LLP agreement clarifies partner rights, duties, and dispute resolution mechanisms. |

| PSC registration mandatory | All People with Significant Control must be registered on the public register in 2026 to comply with UK law. |

| Serious penalties apply | Non-compliance with LLP requirements can result in criminal charges, fines, or imprisonment. |

| Professional advice recommended | Legal guidance ensures your LLP agreement is compliant, tailored to your needs, and protects all partners effectively. |

Understanding an LLP and its benefits

A Limited Liability Partnership represents a hybrid business structure that combines partnership flexibility with limited liability protection for partners’ personal assets. Unlike traditional partnerships where partners face unlimited personal liability for business debts, LLPs shield individual partners from claims against the partnership itself. This legal framework, established under the Limited Liability Partnerships Act 2000, gives you the operational freedom of a partnership whilst protecting your home, savings, and personal property.

LLPs differ significantly from limited companies and traditional partnerships in several ways. In a limited company, directors manage the business on behalf of shareholders, creating a clear separation between ownership and control. Traditional partnerships expose all partners to unlimited liability, meaning creditors can pursue personal assets if the business fails. LLPs occupy the middle ground, offering partnership-style management with corporate-style liability protection. This makes them particularly attractive for professional services firms like solicitors, accountants, and consultants.

The benefits extend beyond liability protection. LLPs offer considerable management flexibility, allowing partners to structure profit sharing, decision making, and operational control according to their specific needs rather than following rigid corporate governance rules. You can tailor voting rights, capital contributions, and exit provisions to suit your partnership’s unique circumstances. Personal asset protection means your house, car, and savings remain safe even if the LLP faces financial difficulties or legal claims.

Pro Tip: LLPs work best for businesses where multiple professionals share expertise and want equal management input whilst protecting personal wealth. If you need external investors or plan to sell shares publicly, a limited company structure may suit you better.

Ideal candidates for LLP structures include professional service providers, family businesses transitioning from traditional partnerships, and collaborative ventures between independent consultants. Understanding why choose LLP structure helps you determine if this model fits your business goals. Comparing types of business structures UK ensures you select the most appropriate legal form for your venture.

Preparing to set up your LLP: legal requirements and documentation

Before forming your LLP, you must satisfy specific statutory requirements and gather essential documentation. Companies House requires formal registration of every LLP operating in the UK, and you cannot legally trade as an LLP until your incorporation is complete. The registration process demands accurate information about your business name, registered office address, and all designated members who will manage the partnership.

Identifying and registering People with Significant Control represents a critical compliance obligation in 2026. Statutory guidance on significant influence defines PSCs as individuals holding more than 25% of surplus assets on winding up, controlling more than 25% of voting rights, or exercising significant influence over the LLP’s management. You must maintain an accurate PSC register and file this information with Companies House, making it publicly accessible through the central register.

Drafting a comprehensive LLP agreement forms the foundation of your partnership’s success. Whilst UK law does not mandate a written agreement, operating without one leaves you vulnerable to disputes and uncertainty. Your agreement should define each partner’s capital contribution, profit and loss sharing ratios, management responsibilities, decision making processes, and procedures for admitting new partners or handling departures. Clear dispute resolution mechanisms prevent costly litigation when disagreements arise.

- Partner eligibility requirements specify that members must be individuals or corporate entities capable of entering legal contracts

- Business name restrictions prohibit offensive terms and require approval if using sensitive words like “royal” or “government”

- Registered office address must be a physical UK location where official correspondence will be sent

- Designated members bear additional responsibilities for filing accounts and maintaining statutory registers

Pro Tip: Appoint at least two designated members to ensure continuity if one becomes unavailable. These individuals carry extra legal duties but do not necessarily hold more power than other partners unless your agreement specifies otherwise.

Filing deadlines demand attention because late submissions trigger automatic penalties. You must register your LLP within a reasonable timeframe of deciding to form it, though no specific deadline applies to initial incorporation. Once registered, annual confirmation statements and accounts face strict deadlines with fines escalating for continued non-compliance. Understanding business registration UK processes and maintaining legal compliance UK professionals standards protects you from unnecessary penalties.

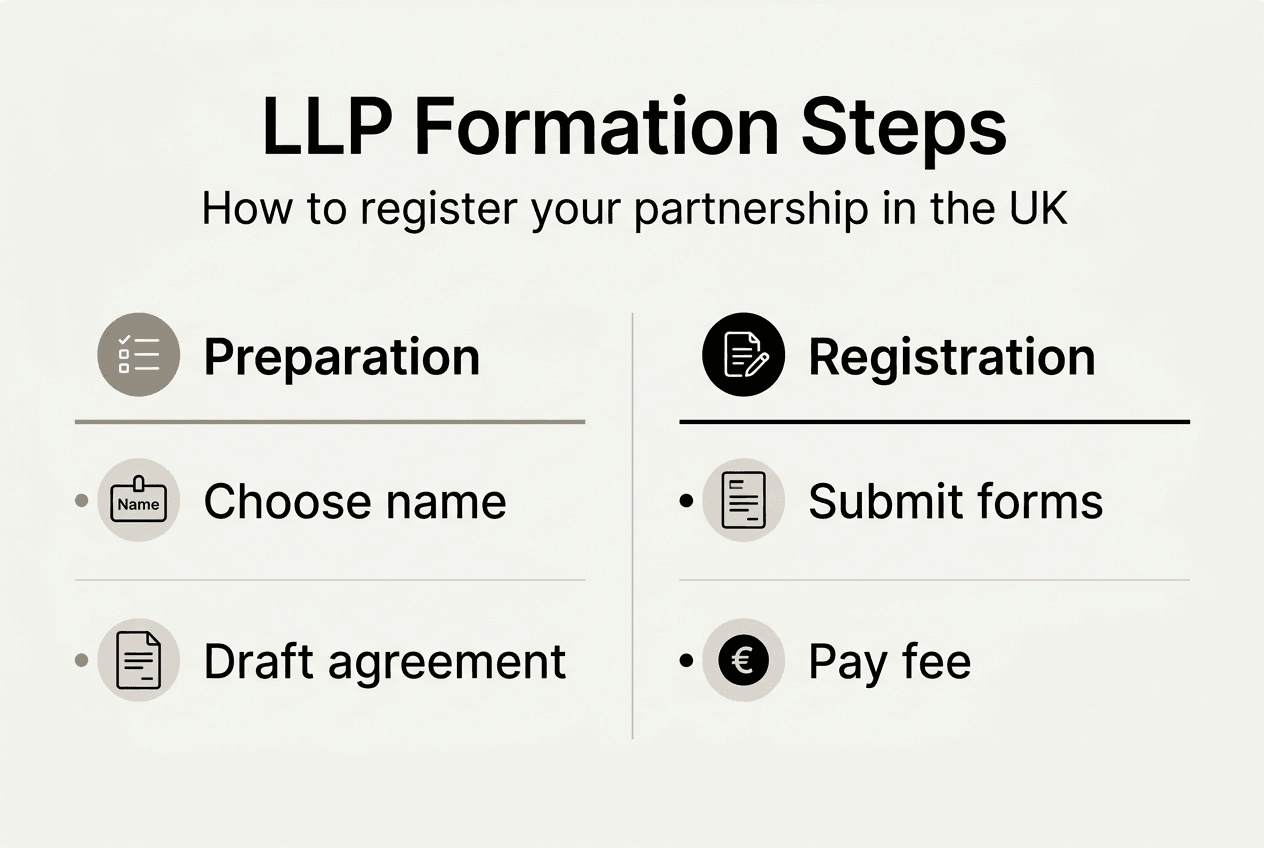

Steps to form and register your LLP in the UK

Forming your LLP requires systematic completion of incorporation documents and submission to Companies House. Follow this structured approach to ensure smooth registration and avoid common pitfalls that delay approval.

-

Choose your LLP name: Select a unique name not already registered or too similar to existing businesses. Check availability through the Companies House name availability checker. Avoid sensitive words requiring additional approvals unless you obtain necessary permissions first.

-

Determine your registered office: Establish a physical address in England, Wales, Scotland, or Northern Ireland where official mail will be delivered. This address becomes public record, so consider using your accountant’s office if you prefer privacy.

-

Identify all members and designated members: List every individual or corporate entity joining the LLP as a member. Designate at least two members to handle statutory filing obligations and maintain registers.

-

Complete Form LL IN01: Submit the incorporation application online through Companies House or by post. Provide your LLP name, registered office, member details, PSC information, and confirmation of compliance with formation requirements.

-

Pay the registration fee: Companies House charges £40 for online applications processed within 24 hours or £100 for same-day incorporation. Postal applications cost £40 with processing taking 8 to 10 days.

-

Draft and execute your LLP agreement: Create a comprehensive agreement outlining partner rights, duties, profit sharing, and decision making processes. LLP agreements are crucial for preventing disputes and clarifying expectations. All members should sign the agreement before commencing business operations.

-

Register People with Significant Control: File PSC details with Companies House and maintain an internal register accessible to authorities. Update this register whenever control changes occur.

Pro Tip: Complete your LLP agreement before submitting incorporation documents. This ensures all members understand their commitments and reduces the risk of disagreements immediately after formation.

| Registration Method | Cost | Processing Time | Best For |

|---|---|---|---|

| Online standard | £40 | 24 hours | Most formations |

| Online same day | £100 | Same working day | Urgent setups |

| Postal application | £40 | 8 to 10 days | No time pressure |

Common pitfalls include choosing names too similar to existing businesses, providing incomplete member information, and failing to register PSCs correctly. Double check all details before submission because errors require resubmission with additional fees. Keep digital copies of all formation documents, including your certificate of incorporation, member agreements, and PSC registers. Following a comprehensive company setup checklist UK and reviewing the start-up checklist UK ensures you complete every necessary step.

Ensuring ongoing compliance and managing your LLP effectively

Maintaining your LLP requires consistent attention to statutory obligations and internal governance. Annual confirmation statements must be filed with Companies House every 12 months, confirming your registered office address, member details, and PSC information remain accurate. Even if nothing changes, you must still file the confirmation statement to avoid penalties. Financial accounts prepared according to applicable accounting standards must be submitted within nine months of your financial year end.

Maintaining the register of People with Significant Control represents an ongoing duty, not a one-time task. Whenever ownership or control changes, you must update your internal PSC register within 14 days and notify Companies House within another 14 days. Failing to comply could result in criminal charges, fines, or imprisonment for responsible members. The severity of these penalties reflects the government’s commitment to corporate transparency and anti-money laundering efforts.

- Late confirmation statements trigger automatic £150 penalties, escalating to £375 for continued delays

- Failure to file accounts results in penalties from £150 to £1,500 depending on delay length

- Inaccurate PSC information can lead to unlimited fines and up to two years imprisonment

- Regular compliance reviews prevent costly mistakes and maintain good standing

Effective LLP agreements help manage partner relationships and prevent disputes from escalating into litigation. Clear provisions addressing profit distribution, decision making authority, and conflict resolution create predictable frameworks for handling disagreements. When partners understand their rights and obligations from the outset, misunderstandings decrease significantly. Regular reviews of your agreement ensure it remains relevant as your business evolves and circumstances change.

| Compliance Task | Frequency | Deadline | Penalty for Non-Compliance |

|---|---|---|---|

| Confirmation statement | Annual | 14 days after review date | £150 minimum |

| Annual accounts | Annual | 9 months after year end | £150 to £1,500 |

| PSC register updates | As needed | 14 days from change | Unlimited fine or imprisonment |

| Member register updates | As needed | Immediate | £150 minimum |

Regularly reviewing and updating your LLP agreement protects against emerging risks and accommodates business growth. Schedule annual reviews where all partners assess whether current provisions still reflect their intentions and business realities. Consider updating your agreement when admitting new members, changing profit sharing arrangements, or expanding into new business areas. Maintaining legal compliance UK standards and understanding legal structures for startups helps you adapt as your business matures. For online businesses, reviewing UK ecommerce compliance risks ensures you address sector-specific requirements.

Enhance your LLP setup with expert resources

Forming your LLP marks the beginning of your business journey, not the end. KefiHub provides comprehensive resources tailored for UK small business owners navigating legal structures, compliance obligations, and operational challenges. Our platform connects you with expert insights on business intelligence UK SMEs need to make informed decisions and compete effectively.

Access our curated legal advice platforms comparison to find professional support for drafting agreements, ensuring compliance, and resolving disputes. Whether you need ongoing legal guidance or one-off document review, our expert-verified recommendations help you choose services matching your budget and requirements. Explore business automation for SMEs to streamline administrative tasks, freeing time for strategic growth activities that drive revenue.

Frequently asked questions

How much does it cost to set up an LLP in the UK?

Registration fees to Companies House range from £40 for standard online applications to £100 for same-day processing. Additional costs include legal fees for drafting your LLP agreement, typically £500 to £2,000 depending on complexity, and ongoing accounting fees for annual compliance. Budget for professional advice to ensure your agreement protects all partners effectively.

Can a company be a member of an LLP in the UK?

Whilst UK law permits corporate members in LLPs, many LLP agreement templates are designed exclusively for individual members. If you want corporate members, you need a specially drafted agreement addressing corporate governance, authorised signatories, and dissolution procedures. Consult a solicitor experienced in partnership law to create appropriate documentation.

What are the penalties for failing to comply with LLP requirements?

Non-compliance may constitute a criminal offence punishable by fines, imprisonment, or both. Late filing penalties start at £150 and escalate with continued delays. Inaccurate PSC information carries unlimited fines and potential imprisonment up to two years. Timely filings and accurate record keeping are essential to avoid these serious consequences.

Do I need a solicitor to draft my LLP agreement?

Whilst not legally required, professional legal advice ensures your agreement complies with current law and addresses your specific circumstances. DIY templates risk missing critical provisions, creating ambiguities that lead to disputes, or including unenforceable clauses. Investing in proper legal drafting prevents costly litigation and protects all partners’ interests effectively.

Recommended

- Why choose LLP structure: benefits and guide for UK 2026 – Kefihub

- Business Registration Step by Step for UK Owners – Kefihub

- Company Setup Checklist for UK Business Success – Kefihub

- Starting a Small Business UK: Step-by-Step Legal Guide – Kefihub

- Qu’est-ce qu’un partenariat informatique ? guide 2026