Buying your first home in the United Kingdom can feel overwhelming once you realise just how many steps happen before the keys are in your hand. For first-time buyers, understanding the legal process of transferring property ownership—known as residential conveyancing—protects you from costly pitfalls and ensures the home you choose is truly yours. This guide breaks down what happens behind the scenes, highlights common mistakes to avoid, and offers practical steps so you can approach your property purchase with clarity and confidence.

Table of Contents

- Residential Conveyancing Explained: Core Concepts

- The Step-By-Step Home Buying Process

- Legal Checks and Essential Searches

- Costs, Fees And Key Financial Risks

- Common Pitfalls For First-Time Buyers

Key Takeaways

| Point | Details |

|---|---|

| Understanding Conveyancing | Residential conveyancing is essential for legally transferring property ownership, ensuring both buyer and seller are protected. |

| Importance of Professional Help | Engage a qualified solicitor or licensed conveyancer to navigate the complexities of the buying process and avoid potential pitfalls. |

| Financial Preparedness is Key | Be aware of all costs involved in the purchase beyond the deposit, including conveyancing fees, searches, and Stamp Duty Land Tax. |

| Avoid Common Mistakes | First-time buyers should get a Mortgage Agreement in Principle early and be thorough in legal checks to prevent costly errors. |

Residential Conveyancing Explained: Core Concepts

Residential conveyancing is the legal process of transferring property ownership from seller to buyer. It’s far more than just signing papers—it’s a comprehensive system that protects both parties and ensures the transaction is legitimate and binding.

At its core, residential conveyancing involves legal work to support the purchase and sale of property. This includes verifying that the seller actually owns what they’re selling, checking for any hidden problems with the property, and ensuring all financial obligations are clear before you commit.

The process protects your interests by confirming your legal rights to the property once you’ve paid for it. Without conveyancing, you could hand over your money and discover the seller doesn’t have the right to sell the house to you—a nightmare scenario that formal conveyancing prevents.

Here are the main components of residential conveyancing:

- Title verification – Confirming the seller owns the property and has the legal right to sell it

- Property searches – Uncovering potential issues like flooding risks, planning breaches, or environmental concerns

- Contract management – Drafting and reviewing agreements that outline both parties’ rights and obligations

- Financial settlement – Arranging the money transfer and ensuring all debts attached to the property are paid

- Legal completion – The final step where ownership officially passes to you

The entire process is typically handled by solicitors or licensed conveyancers—qualified professionals who understand property law and can spot potential problems. They act as your intermediary, communicating with the seller’s legal representative and ensuring nothing falls through the cracks.

Conveyancing is your safety net. It confirms you own what you’re buying and identifies issues before you’ve committed your money.

You might wonder why this process exists at all. The answer is straightforward: property is the biggest purchase most people make in their lifetime. The conveyancing system ensures that transaction is legally sound, financially protected, and properly documented. Without it, the property market would collapse into chaos and disputes.

First-time buyers often underestimate how much happens behind the scenes during conveyancing. Searches alone can reveal whether a property is in a flood zone, subject to planning restrictions, or has outstanding council tax issues. These aren’t minor details—they directly affect your property’s value and your ability to sell it later.

The timeline matters too. Conveyancing can take weeks or months depending on how quickly both parties respond and whether any issues emerge. Understanding this upfront helps you plan your move and avoid unrealistic expectations.

Pro tip: Ask your conveyancer to explain the timeline and key milestones in writing at the start—knowing when each stage happens removes stress and helps you prepare for completion day.

The Step-By-Step Home Buying Process

Buying a home in the UK follows a structured journey with distinct stages. Understanding each step helps you stay organised, manage timelines, and avoid costly mistakes along the way.

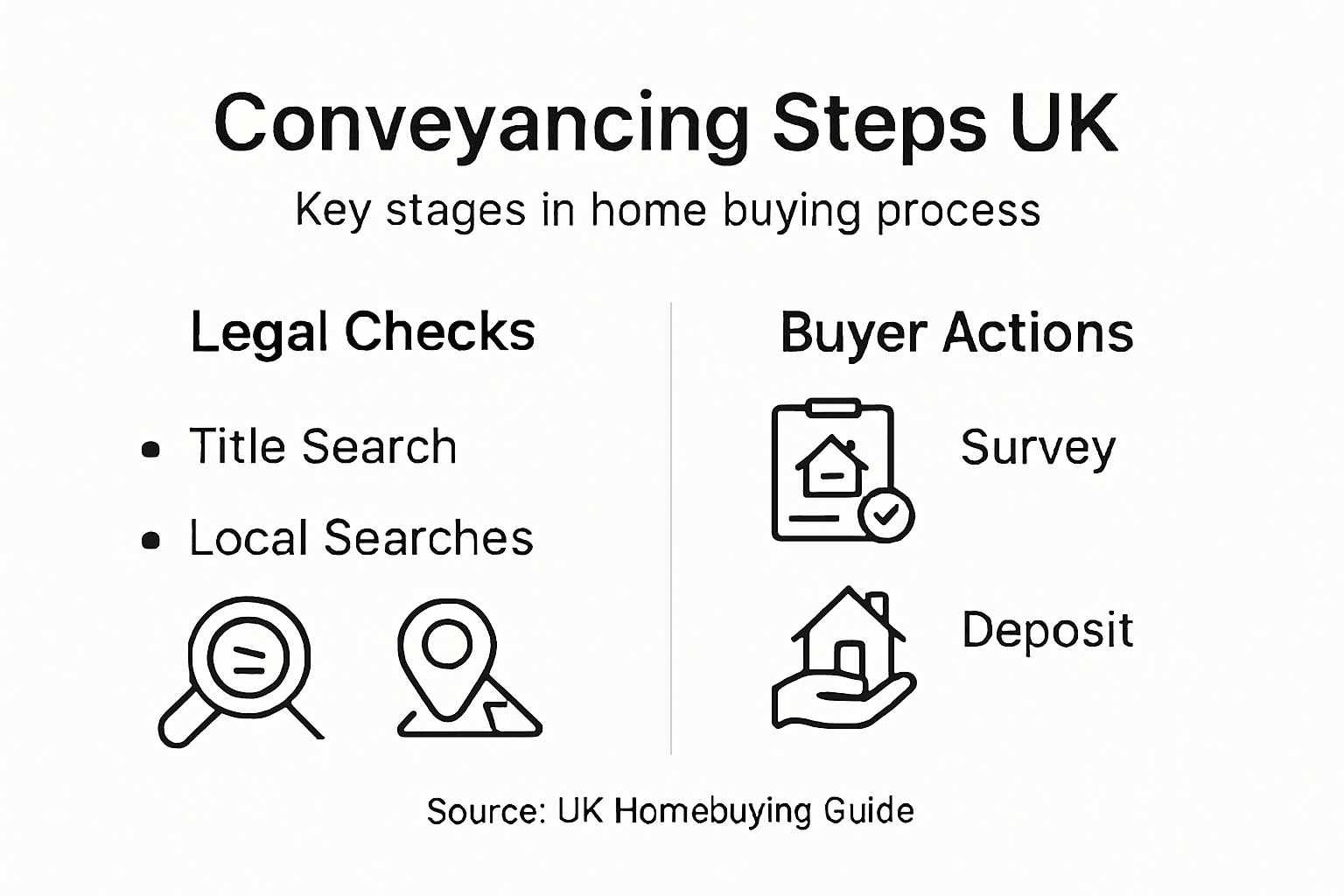

The process begins with financial preparation. Before you view a single property, assess what you can afford and obtain a mortgage agreement in principle from your lender. This document shows sellers you’re a serious buyer and gives you clarity on your budget.

Next comes the exciting part—property hunting and making an offer. Once you find a property you like, you submit an offer. If accepted, you’ve reached a crucial turning point, but you’re not legally bound yet.

After your offer is accepted, the home buying process requires hiring a conveyancer or solicitor to handle the legal side. They conduct searches and investigations into the property’s history and condition.

Here’s what happens in the middle stages:

- Instruct a solicitor or conveyancer to begin legal checks

- Arrange a survey to assess the property’s physical condition

- Complete formal mortgage approval with your lender

- Review all search results and survey findings with your conveyancer

- Negotiate any issues that arise from searches or surveys

Once everything checks out, you reach contract exchange. Both parties sign contracts, which legally binds you to the purchase. At this point, you’ve committed your deposit and cannot withdraw without losing it.

Contract exchange is the moment the deal becomes legally binding. After this point, backing out costs you money.

The final stage is completion. Your solicitor transfers the remaining funds to the seller’s solicitor, and ownership officially passes to you. You receive the keys and the property is yours.

The entire process typically takes 8–12 weeks, though this varies depending on how quickly each party responds and whether complications arise. Chain delays—where your purchase depends on the seller’s own purchase completing—can extend timelines significantly.

First-time buyers often underestimate how many moving parts exist. Surveys, searches, mortgage approvals, and conveyancing all happen simultaneously, and delays in any area can slow everything down.

Pro tip: Keep a checklist of key dates from your conveyancer and set reminders two weeks before each deadline—this prevents last-minute panics and ensures nothing slips through the cracks.

Legal Checks and Essential Searches

Once your offer is accepted, your conveyancer begins a thorough investigation into the property. This stage is critical—it uncovers hidden problems that could affect your investment, safety, or ability to sell later.

Your conveyancer will conduct several standard searches to investigate the property’s history and any legal issues. These searches check local authority records, environmental risks, flooding patterns, and planning applications affecting the property.

Property searches reveal potential issues like whether the area floods regularly, if planned developments nearby will affect your view or noise levels, or if previous owners made illegal alterations to the building. Some searches can save you from buying a property with serious hidden defects.

Here are the main searches your conveyancer will order:

- Local Authority Search – Reveals planning breaches, building regulation violations, and enforcement action against the property

- Environmental Search – Identifies flooding risks, ground stability issues, and historical industrial uses

- Water and Drainage Search – Confirms water and sewage connections and identifies any flooding from water sources

- Coal Authority Search – Needed only in mining areas; checks for subsidence risks from historic mining

- Chancel Repair Search – Checks if you’re liable for church chancel repairs (rare but essential)

Beyond searches, your conveyancer also verifies the seller’s identity and confirms they legally own the property. This involves checking the property title documents held at the Land Registry, which prove ownership and reveal any restrictions or mortgages affecting the property.

Your conveyancer will also check for title defects—legal issues that could prevent you from owning the property freely. These might include rights of way that allow neighbours to cross your land, covenants restricting how you use the property, or unresolved mortgages from previous sales.

Missing or incomplete searches can lead to expensive problems after purchase. Your conveyancer protects you by being thorough upfront.

The process typically takes 2–4 weeks, depending on how quickly local authorities respond. Some searches return within days; others take longer. Your conveyancer will chase slow responses to keep the timeline on track.

If searches reveal issues, don’t panic. Minor findings are common. Your conveyancer advises you on what matters and what doesn’t, and you can often renegotiate the price or ask the seller to fix problems before completion.

Pro tip: Request copies of all search results and title documents from your conveyancer before exchange of contracts—reviewing these yourself gives you peace of mind and shows you understand what you’re buying.

Costs, Fees and Key Financial Risks

Conveyancing isn’t free. Understanding the costs upfront helps you budget properly and avoids surprises when bills arrive. Most first-time buyers underestimate how many fees stack up during the purchase process.

Your conveyancer’s fees typically range from £800 to £2,000 depending on the property price and complexity. Some charge a flat rate; others calculate fees as a percentage of the purchase price. Always ask for a written quote before you instruct them.

Beyond conveyancing fees, you’ll pay for several searches and checks:

- Local Authority Search: £100–£200

- Environmental Search: £50–£150

- Water and Drainage Search: £50–£100

- Other specialist searches: £50–£300 depending on location

- Mortgage lender’s fees: Typically £100–£500

- Survey costs: £300–£1,500 depending on property size and survey type

There’s also Stamp Duty Land Tax (SDLT), a government tax on property purchases. First-time buyers benefit from relief on properties up to £425,000, but you’ll pay tax on anything above that threshold at rates between 5% and 12%.

Beyond these direct costs, several financial risks can derail your purchase. If your mortgage lender reduces their offer after the survey reveals problems, you might need to renegotiate or withdraw. This leaves you out of pocket for searches and surveys you’ve already paid for.

Hidden defects discovered late can cost thousands to fix. Thorough conveyancing now prevents expensive problems later.

Chain delays are another risk. If the seller’s own purchase falls through, your completion date shifts indefinitely. You’ve committed your deposit but can’t move in, creating stress and potential accommodation costs.

Some buyers face gazumping—where the seller accepts a higher offer after yours—though this is less common now. Similarly, gazundering happens when the buyer reduces their offer just before completion, exploiting the seller’s desperation to complete.

Another risk involves unforeseen repairs. Even thorough surveys can miss issues. Budget 5–10% of the purchase price for unexpected repairs in the first year, especially for older properties.

Finally, missing the completion deadline costs money. Your mortgage offer might expire, or bridge finance fees might apply if you need temporary funding.

To help you understand the financial aspects of buying a home, here is a quick summary of typical conveyancing costs and related expenses:

| Cost Type | Typical Range | Who Pays | Impact on Budget |

|---|---|---|---|

| Conveyancer’s Fees | £800–£2,000 | Buyer | Major upfront cost |

| Property Searches | £100–£300 | Buyer | Essential for due diligence |

| Survey Costs | £300–£1,500 | Buyer | Reveals hidden issues |

| Stamp Duty Land Tax | 0%–12% (above threshold) | Buyer | Significant for high-value properties |

| Mortgage Fees | £100–£500 | Buyer | Linked to loan approval |

| Unexpected Repairs | 5–10% of purchase price | Buyer | Often overlooked, affects future spending |

Pro tip: Get everything in writing from your conveyancer—fees, timeline, what’s included, and what costs extra—before you commit, and compare quotes from at least two conveyancers to ensure competitive pricing.

Common Pitfalls for First-Time Buyers

First-time buyers often make preventable mistakes that cost money, delay completion, or leave them exposed to legal risks. Knowing what to avoid puts you ahead of the curve.

One critical mistake is skipping the Mortgage Agreement in Principle. This document proves to sellers that you can actually afford the property. Without it, your offer gets rejected, wasting time and damaging your reputation with estate agents.

Common pitfalls include rushing legal checks and underestimating costs beyond the deposit. Many buyers focus only on the purchase price and ignore the mountain of additional expenses—surveys, searches, conveyancing fees, and taxes. This leaves them scrambling for money later.

Here are the pitfalls that trip up most first-time buyers:

- Skipping the Mortgage Agreement in Principle and making weak offers

- Underestimating total costs and budgeting only for the deposit

- Ignoring location factors like transport links, schools, and flood risks

- Rushing through legal checks and conveyancing to speed up the process

- Viewing properties without proper preparation or guidance

- Accepting the first survey without understanding what it covers

- Not reading contracts carefully or asking questions about unfamiliar terms

Another common mistake is ignoring location factors. A cheap property in a poor location might seem like a bargain, but it could damage your future resale value. Things like noisy neighbours, planned developments, flooding risks, or poor transport links matter far more than you realise.

Many buyers also rush the conveyancing process. Pressuring your conveyancer to move faster increases the risk that important issues get missed. Thorough conveyancing takes time, but it’s worth it.

Rushing conveyancing to save a few weeks can cost thousands in hidden problems discovered after purchase.

Some buyers fail to engage qualified legal professionals early enough. Instructing a conveyancer only after your offer is accepted means you’ve already missed opportunities to ask questions about the property or negotiate better terms.

Another pitfall is not understanding the legal language used in contracts and searches. Terms like “restrictive covenants,” “easements,” and “title defects” confuse buyers who don’t ask for explanations. This leaves them vulnerable to agreeing to terms they don’t understand.

Finally, buyers sometimes make offers without properly viewing the property or without understanding what surveys reveal. A cheap survey misses problems; an expensive survey sometimes reveals issues that require renegotiation or withdrawal.

Here is a reference table outlining common pitfalls for first-time buyers and how to avoid them:

| Pitfall | Consequence | How to Avoid |

|---|---|---|

| Lack of mortgage pre-approval | Offer may be rejected | Obtain Agreement in Principle early |

| Ignoring location quality | Poor resale value | Research area and future developments |

| Rushing legal checks | Missed issues, costly fixes | Allow sufficient time for conveyancing |

| Underestimating total fees | Budget shortfall | Calculate all buying costs in advance |

| Accepting contracts blindly | Legal risks | Seek explanations for unclear terms |

Pro tip: Get a Mortgage Agreement in Principle before viewing properties, budget for all costs upfront including searches and legal fees, and instruct your conveyancer as soon as your offer is accepted—not after.

Secure Your Home Buying Journey with Expert Guidance from KefiHub

Navigating the complexities of residential conveyancing can feel overwhelming, especially with key challenges like understanding legal checks, managing conveyancing timelines and budgeting for all associated costs. Many first-time buyers struggle with terms such as “title verification” and “contract exchange” that are critical to ensuring a smooth and secure property purchase. At KefiHub, we understand these pain points and provide clear, practical advice tailored to help UK homebuyers avoid common pitfalls and make informed decisions.

Ready to take control of your home buying process and avoid costly mistakes? Explore our expert insights on conveyancing and legal home buying at KefiHub. Get the essential knowledge you need about property searches and legal checks, understand crucial steps like contract exchange, and budget wisely to protect your investment. Visit us today and empower your property journey with trusted, actionable guidance.

Frequently Asked Questions

What is residential conveyancing?

Residential conveyancing is the legal process of transferring property ownership from seller to buyer, involving checks and paperwork to ensure a legitimate transaction.

Why is conveyancing important when buying a home?

Conveyancing is important because it verifies the seller’s ownership, uncovers potential problems with the property, and ensures all legal rights and financial obligations are clear before committing to a purchase.

How long does the conveyancing process usually take?

The conveyancing process typically takes 8–12 weeks, depending on how quickly both parties respond, and can be extended by issues such as chain delays or complications in searches.

What costs are involved in the conveyancing process?

Costs can include conveyancer fees (£800 to £2,000), searches (£100 to £300), survey costs (£300 to £1,500), and Stamp Duty, among other fees. It’s essential to budget for these additional expenses beyond the deposit.

Recommended

- How to Find Reliable Legal Advice for UK Homebuyers – Kefihub

- 7 Essential Conveyancing Tips UK Professionals Must Know – Kefihub

- 7 Essential Conveyancing Tips UK Professionals Must Know – Kefihub

- 7 Key Stages of Conveyancing Every UK Professional Should Know – Kefihub

- Understanding the UK’s 2025 Airbnb & short-term rental law changes

- Moving into Historic Portsmouth Homes | A Local Buyer’s & Moving Guide

")