Many UK property buyers and sellers wrongly assume valuation simply mirrors asking price or online estimates. This confusion leads to poor offers, unrealistic expectations, and costly mistakes. Understanding how professional valuation works empowers you to negotiate confidently, price accurately, and invest wisely. This guide demystifies property valuation methods, explains who performs them, and shows how to apply this knowledge when buying, selling, or investing in UK property during 2026.

Table of Contents

- What Is Property Valuation And Why Does It Matter?

- Common Property Valuation Methods Used In The UK

- Who Carries Out Property Valuations And What Affects Their Accuracy?

- Applying Property Valuation Knowledge For Buying, Selling, And Investing

- Explore Our UK Property Investment Resources

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Valuation estimates market worth | Professional valuation assesses a property’s true market value based on location, condition, and comparable sales data. |

| Different purposes require different valuations | Mortgage, sale, and tax valuations serve distinct purposes with varying assessment criteria and results. |

| RICS surveyors provide trusted assessments | Chartered surveyors qualified by RICS follow UK standards to deliver accurate, credible property valuations. |

| Valuation informs smarter property decisions | Understanding valuation helps buyers avoid overpaying, sellers set realistic prices, and investors evaluate returns. |

What is property valuation and why does it matter?

Property valuation estimates what a residential property is worth at a specific point in time. It’s not simply the price a seller hopes to achieve or what an online calculator suggests. Instead, property valuation determines market value based on rigorous analysis of location, condition, size, and comparable recent sales nearby.

Valuation matters enormously when you’re navigating UK property transactions. Lenders require mortgage valuations before approving loans to ensure the property secures the debt. Sellers need accurate valuations to set competitive asking prices that attract serious buyers without leaving money on the table. Buyers rely on valuations to make informed offers and avoid overpaying in heated markets. Investors use valuations to assess potential returns and identify undervalued opportunities.

Common misconceptions create confusion and poor decisions. Many people conflate asking price with actual market value, assuming the seller’s number reflects true worth. Others trust automated online estimates without recognising these tools lack property-specific details like condition, renovations, or neighbourhood nuances. Some buyers expect valuations to match their budget rather than market reality.

Several factors influence how valuers arrive at their figures:

- Location drives value significantly, with desirable postcodes, good transport links, and quality schools commanding premiums.

- Property size and layout affect value, including number of bedrooms, bathrooms, and usable living space.

- Condition and age matter, as well-maintained properties with modern fittings typically achieve higher valuations than dated, neglected homes.

- Market trends shape valuations, with local supply, demand, and economic conditions influencing what buyers will pay.

- Comparable sales provide evidence, as recent transactions of similar properties nearby set valuation benchmarks.

The UK property market recognises three main types of valuation. Market valuation estimates what a willing buyer would pay a willing seller in current conditions. Mortgage valuation assesses whether a property provides adequate security for the lender’s loan amount. Tax valuation determines property worth for inheritance tax, capital gains tax, or council tax purposes.

Pro tip: Always commission an independent valuation before making a property offer, even if the lender arranges a separate mortgage valuation. This protects you from overpaying and strengthens your negotiating position with evidence-based figures.

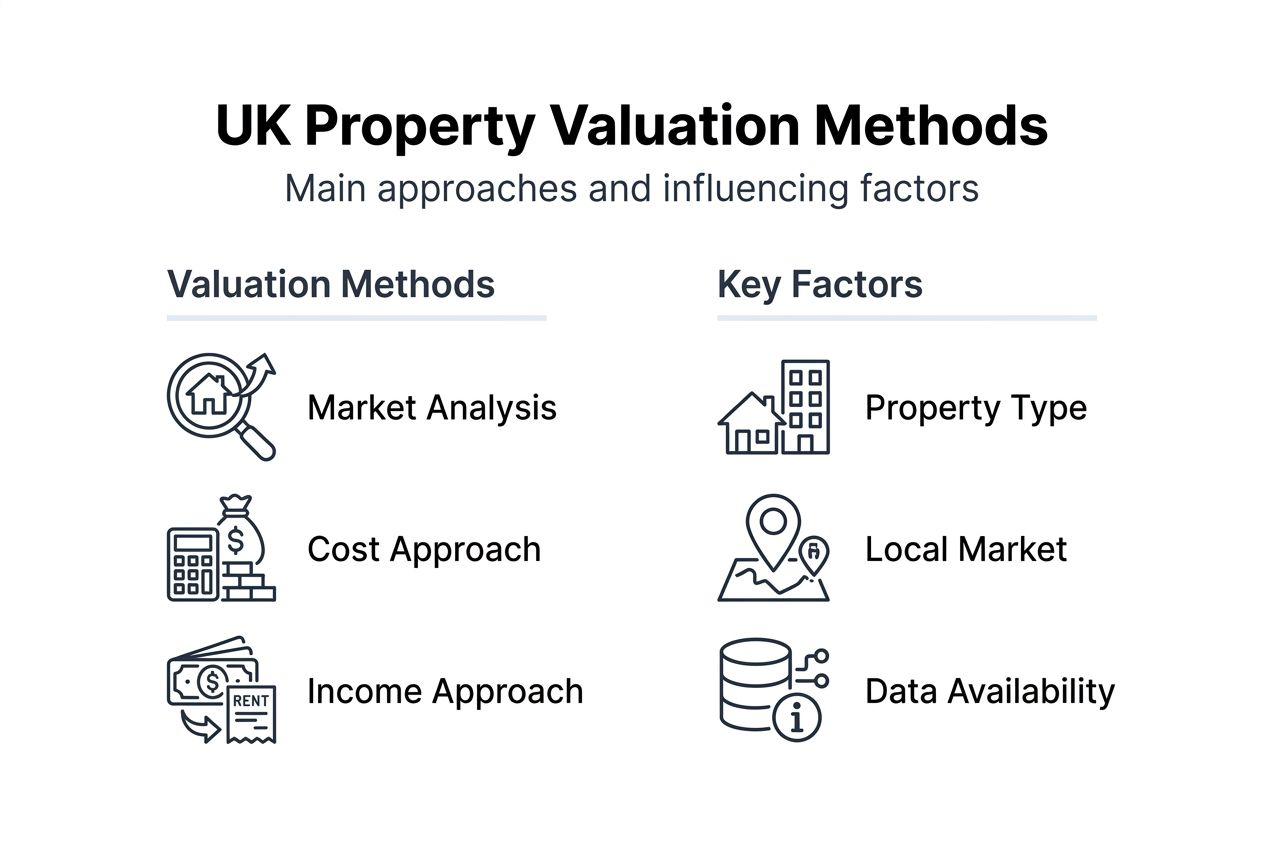

Common property valuation methods used in the UK

Professional valuers employ several established methods depending on property type and valuation purpose. Understanding these approaches helps you interpret valuation reports and ask informed questions.

Comparative market analysis dominates residential property valuation across the UK. Valuers identify similar properties sold recently in the same neighbourhood, typically within the past three to six months. They adjust prices for differences in size, condition, features, and exact location to estimate what your property would achieve in today’s market. This method works best when sufficient comparable sales exist and market conditions remain stable.

The cost approach calculates what rebuilding the property from scratch would cost, then subtracts depreciation for age and wear. This method suits unique properties, new builds, or insurance valuations where comparable sales prove scarce. However, it often produces lower figures than market valuations because it ignores location premium and market sentiment.

The income approach values investment properties based on rental income potential. Valuers estimate achievable annual rent, apply a capitalisation rate reflecting market yields and risk, and derive capital value. Buy-to-let investors rely heavily on this method to assess whether purchase prices align with expected returns. Commercial properties almost always use income-based valuations.

| Method | Best suited for | Key limitation |

|---|---|---|

| Comparative market analysis | Standard residential sales | Requires recent comparable sales data |

| Cost approach | Unique properties, new builds | Ignores location premium and market demand |

| Income approach | Buy-to-let, commercial property | Depends on accurate rental projections |

Professional valuers rarely rely on a single method. Instead, they combine approaches to cross-check results and improve accuracy. A residential valuation might use comparative analysis as primary evidence whilst referencing cost approach figures to validate the conclusion. Investment property valuations often blend income and comparative methods to assess both yield and capital appreciation potential.

Key factors affecting method selection include property type, local market activity, data availability, and valuation purpose. In active markets with frequent transactions, comparative analysis dominates. In thin markets or for unusual properties, valuers lean more heavily on cost or income approaches.

Who carries out property valuations and what affects their accuracy?

RICS-qualified chartered surveyors represent the gold standard for UK property valuations. RICS qualification demonstrates professional competence through rigorous training, examinations, and adherence to strict ethical standards. When instructing a valuer for mortgage, legal, or investment purposes, always verify RICS membership to ensure credible results.

Estate agents often provide informal valuations when you’re considering selling. Whilst helpful for initial guidance, these lack the independence and rigour of formal RICS valuations. Agents may inflate figures to win instructions or please vendors, creating unrealistic expectations that delay sales.

Several factors determine valuation accuracy and reliability:

- Valuer experience and local knowledge significantly impact assessment quality, as understanding neighbourhood nuances improves comparable selection and adjustment judgements.

- Property inspection thoroughness matters enormously, with detailed physical examinations revealing condition issues that desk-based reviews miss entirely.

- Market data quality and recency affect accuracy, as valuers need comprehensive, up-to-date transaction records to identify true comparables and trends.

- Economic conditions and market volatility introduce uncertainty, making valuations during rapid price changes inherently less precise than stable market assessments.

- Valuation purpose influences approach, as mortgage valuations prioritise downside protection whilst market valuations seek achievable sale prices.

Different valuation types produce varying figures for the same property. Mortgage valuations often come in lower than market valuations because lenders adopt conservative assumptions to protect against default risk. Tax valuations may differ again, reflecting specific regulatory definitions and assumptions required by HMRC guidance.

Pro tip: When comparing multiple valuations, focus on the methodology and evidence each valuer used rather than simply choosing the highest or lowest figure. Understanding how they reached their conclusion reveals which assessment deserves most confidence.

External factors beyond the valuer’s control also influence results. Local market sentiment shifts rapidly with economic news, interest rate changes, or planning decisions. National housing policy, tax treatment, and lending criteria shape what buyers can and will pay. Seasonal variations affect demand, with spring typically seeing higher activity and prices than winter months.

Professional, independent valuations provide the most trustworthy figures precisely because qualified surveyors have no vested interest in inflating or deflating values. They stake their professional reputation and regulatory standing on delivering honest, evidence-based assessments.

Applying property valuation knowledge for buying, selling, and investing

Understanding valuation empowers smarter decisions across every property transaction scenario you’ll encounter.

When buying, commission your own valuation before making offers on properties you’re seriously considering. This investment, typically £300 to £600 depending on property value and complexity, prevents costly mistakes. Compare the valuation against the asking price to identify overpriced properties where negotiation scope exists. Accurate valuation helps avoid overpaying and supports confident offers backed by professional evidence.

For sellers, obtain a formal valuation before setting your asking price rather than relying solely on estate agent opinions. Realistic pricing based on solid evidence attracts serious buyers quickly, whilst overpricing based on optimistic guesses leads to prolonged marketing, price reductions, and ultimately lower achieved prices. Review comparable sales your valuer identified to understand how your property stacks up and where improvements might add value.

Investors should always evaluate rental yield against purchase price using professional valuations. Calculate annual rent as a percentage of the valuation figure to assess whether returns justify the investment given mortgage costs, maintenance, and void periods. Compare yields across different properties and locations to identify the best opportunities. Valuation also helps investors spot undervalued properties where renovation or repositioning could unlock significant capital appreciation.

Negotiation benefits enormously from valuation knowledge:

- Present professional valuation evidence to support your offer when it falls below asking price, demonstrating your position reflects market reality rather than bargaining tactics.

- Identify specific comparable sales that justify your valuation, referencing exact addresses, sale dates, and prices to build credibility.

- Highlight any condition issues or needed repairs the valuation uncovered, using these to negotiate price reductions or request the seller address problems before completion.

- Understand the seller’s position by researching how long the property has been marketed and whether previous price reductions suggest flexibility.

- Use mortgage valuation results as additional leverage if the lender’s figure comes in below asking price, creating urgency for the seller to accept realistic offers.

Professional valuations reduce transaction risk significantly. They reveal structural issues, boundary disputes, or legal complications early in the process when you can still withdraw or renegotiate. They provide lenders with confidence to approve mortgages at appropriate loan-to-value ratios. They create audit trails for tax purposes, documenting property values at acquisition for future capital gains calculations.

“The best property decisions combine emotional appeal with financial discipline. Professional valuation provides the objective foundation that keeps enthusiasm grounded in market reality, protecting both your capital and future returns.”

Explore our UK property investment resources

Now that you understand how property valuation works and why it matters, you’re ready to apply this knowledge confidently. To deepen your expertise and explore related topics, KefiHub offers comprehensive resources tailored for UK property buyers, sellers, and investors.

Our detailed property investment guide walks you through every stage of building a successful UK property portfolio, from identifying opportunities to managing tenants effectively. If you’re navigating the legal complexities of property purchase, discover how to find reliable legal advice that protects your interests throughout the transaction.

For those just starting their investment journey, our step-by-step property investment guide breaks down the entire process into manageable actions, helping you avoid common pitfalls and accelerate your progress.

Frequently asked questions

What is the difference between market value and asking price?

Market value represents the estimated price a willing, informed buyer would pay a willing seller in current market conditions, based on professional analysis of comparable sales and property characteristics. Asking price is simply the amount the seller chooses to advertise, which may be set higher than market value to allow room for negotiation or lower to attract quick offers.

How often should I get my property valued?

Property owners should obtain professional valuations when buying, selling, refinancing, or undertaking major renovations that might significantly alter value. Buy-to-let investors benefit from periodic valuations every three to five years to monitor portfolio performance, assess equity growth, and inform refinancing decisions. Market conditions matter too, with valuations becoming more important during periods of rapid price change.

Can online valuation tools replace professional appraisals?

Online automated valuation models provide quick estimates based on property records, land registry data, and statistical algorithms, but they lack the nuance and accuracy of professional appraisals. They cannot account for property-specific factors like condition, recent improvements, unusual features, or micro-location advantages. For important decisions like purchase offers, mortgage applications, or tax reporting, always commission a qualified surveyor’s valuation.

What qualifications should a property valuer have in the UK?

Seek valuers who hold RICS chartered surveyor status, which demonstrates professional competence through rigorous qualification requirements and ongoing professional development. RICS members follow strict valuation standards, maintain professional indemnity insurance, and adhere to ethical codes that protect clients. For mortgage or legal purposes, lenders and solicitors typically require RICS-qualified valuations to ensure credibility and compliance with UK standards.

Recommended

- Property Investment Explained: A Complete UK Guide – Kefihub

- Property Investment Step by Step for UK Beginners – Kefihub

- Property Investment Guide UK: Secure Your First Buy – Kefihub

- Rental income taxation in Portugal: 2026 guide – RIVA PRIME CONSULTING