Safeguarding your business from financial crime means more than just confirming a client’s name. UK law requires every business owner to go beyond the basics with anti-money laundering checks that are much more thorough than simple identification. These checks protect you from serious risks and ensure you meet strict legal requirements. This guide breaks down the essentials, helping you understand what regulators expect and what practical steps keep your business secure and compliant.

Table of Contents

- What Are Anti-Money Laundering Checks?

- Types Of AML Checks And Their Differences

- Legal Framework And 2026 Regulatory Updates

- Your Business Obligations And Key Roles

- Common Pitfalls And How To Avoid Them

- Costs, Penalties, And Staying Compliant

Key Takeaways

| Point | Details |

|---|---|

| Mandatory AML Checks | Anti-money laundering checks are essential legal requirements for businesses to combat financial crime through customer verification and transaction monitoring. |

| Types of Due Diligence | Businesses must differentiate between Standard, Enhanced, and Simplified Due Diligence to manage varying risk levels effectively. |

| Role of Technology | Investing in digital AML verification tools can enhance compliance efficiency and reduce manual processing time. |

| Consequences of Non-Compliance | Non-compliance can lead to severe financial penalties and reputational damage, making proactive compliance essential for business integrity. |

What Are Anti-Money Laundering Checks?

Anti-money laundering (AML) checks are critical legal processes designed to protect businesses and financial systems from criminal financial activities. These systematic procedures help organisations identify, prevent, and report potential money laundering risks by thoroughly examining customer transactions and identities.

Under UK regulations, businesses must implement comprehensive AML verification processes that go beyond simple customer identification. These checks involve multiple strategic components:

- Verifying customer identities

- Assessing transaction risks

- Monitoring financial activities

- Reporting suspicious transactions

- Maintaining detailed documentation

The primary objective of these checks is to create robust barriers against financial criminals attempting to disguise illegally obtained funds as legitimate income. By requiring businesses to conduct due diligence, the UK government ensures a structured approach to detecting and preventing potential financial crimes.

Money laundering checks are not optional – they are mandatory legal requirements for numerous professional sectors, including financial services, accounting firms, legal practices, and estate agencies. Regulated businesses must register for supervision, appoint responsible officers, and establish comprehensive risk assessment frameworks to remain compliant.

AML checks are your first line of defence against sophisticated financial criminal activities.

Key Components of AML Verification include:

- Customer Identity Verification

- Risk Profile Assessment

- Ongoing Transaction Monitoring

- Suspicious Activity Reporting

- Record Keeping and Documentation

These processes help businesses understand their customers’ financial behaviours, detect unusual patterns, and prevent potential criminal exploitation of financial systems. AML compliance requirements are designed to be comprehensive and adaptable to evolving financial crime techniques.

Pro tip: Invest in robust digital AML verification tools that can automate complex compliance checks and reduce manual processing time.

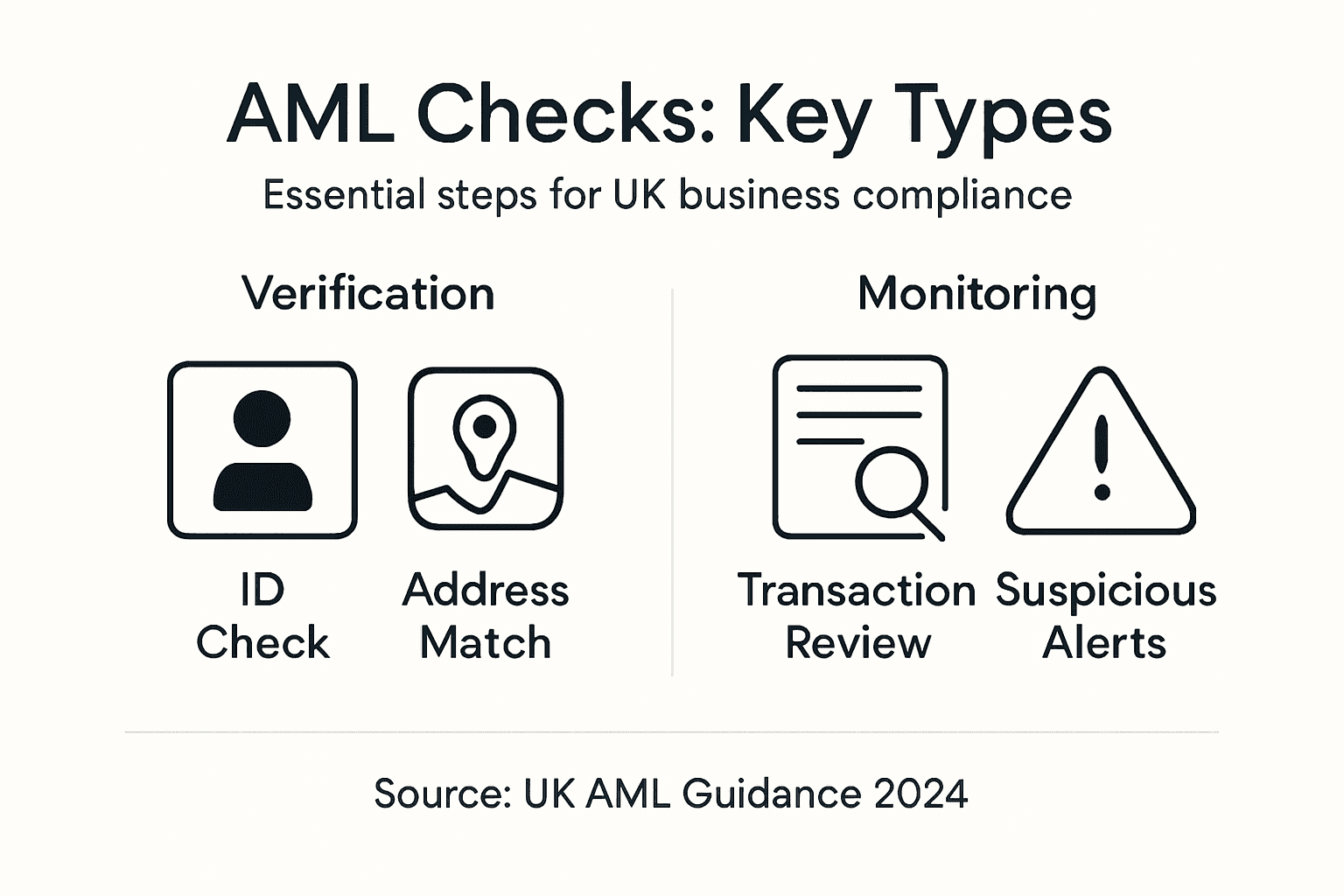

Types Of AML Checks And Their Differences

Anti-money laundering (AML) checks are not one-size-fits-all processes. Instead, they comprise multiple sophisticated verification strategies tailored to different risk levels and business contexts. Understanding these variations is crucial for organisations seeking comprehensive financial protection.

The primary categories of AML checks include customer due diligence measures, which are strategically designed to assess and mitigate potential financial risks:

- Standard Customer Due Diligence (CDD): Basic identity verification

- Enhanced Due Diligence (EDD): Deeper background investigations

- Simplified Due Diligence (SDD): Lower-risk transaction checks

Customer Due Diligence (CDD) represents the foundational level of AML verification. These checks involve collecting and verifying essential customer information, including:

- Full legal name

- Residential address

- Date of birth

- Photographic identification

- Proof of tax identification

Enhanced Due Diligence (EDD) becomes necessary when dealing with higher-risk scenarios. These more rigorous Know Your Customer checks involve:

- Investigating source of funds

- Conducting extensive background checks

- Scrutinising transactions from high-risk jurisdictions

- Verifying beneficial ownership structures

- Assessing potential politically exposed persons (PEPs)

Effective AML checks are not about creating barriers, but building trust through transparent financial practices.

The complexity and depth of AML checks depend on several critical factors, including:

Here is a comparison of AML check types and their business implications:

| AML Check Type | Typical Use Case | Depth of Verification | Impact on Business |

|---|---|---|---|

| Standard Due Diligence (CDD) | Routine financial transactions | Basic identity confirmation | Maintains compliance |

| Enhanced Due Diligence (EDD) | High-risk customer scenarios | Extensive background screening | Reduces exposure to risk |

| Simplified Due Diligence (SDD) | Low-risk, small-value transactions | Minimal documentation | Speeds up onboarding |

- Customer risk profile

- Transaction value

- Geographic location

- Business relationship nature

- Industry-specific regulations

Pro tip: Develop a flexible AML verification framework that can dynamically adjust check intensity based on real-time risk assessments.

Legal Framework And 2026 Regulatory Updates

The UK’s anti-money laundering legal landscape continues to evolve, with comprehensive regulatory updates designed to combat increasingly sophisticated financial crimes. The primary legislative foundation remains the Money Laundering, Terrorist Financing and Transfer of Funds Regulations, which undergo continuous refinement to address emerging economic challenges.

Key developments in the 2026 regulatory framework focus on several critical areas:

- Strengthening supervisory oversight

- Enhancing risk-based compliance approaches

- Improving cross-sector coordination

- Expanding technological monitoring capabilities

- Increasing penalties for non-compliance

Regulatory Scope now extends across multiple professional sectors, including:

- Financial services

- Legal practices

- Accounting firms

- Estate agencies

- Cryptocurrency exchanges

The 2017 Regulations established fundamental compliance requirements, with 2026 updates introducing more nuanced and technologically advanced verification processes. These changes reflect the UK’s commitment to aligning with international anti-money laundering standards and addressing increasingly complex financial crime methodologies.

Compliance is not just a legal obligation, but a critical component of financial system integrity.

Businesses must now implement more sophisticated risk assessment mechanisms, including:

- Advanced customer due diligence protocols

- Real-time transaction monitoring systems

- Comprehensive beneficial ownership investigations

- Enhanced reporting mechanisms

- Continuous staff training programmes

The regulatory landscape demands a proactive approach, with businesses expected to demonstrate robust internal controls and a demonstrable commitment to preventing financial crimes.

Pro tip: Invest in adaptable compliance technology that can quickly integrate new regulatory requirements and provide comprehensive risk management capabilities.

Your Business Obligations And Key Roles

Every UK business operating in regulated sectors must navigate complex anti-money laundering responsibilities. These obligations extend far beyond simple paperwork, demanding a comprehensive approach to financial governance and risk management.

Key Compliance Roles within an organisation include:

- Money Laundering Reporting Officer (MLRO): Primary compliance champion

- Senior Management: Strategic oversight and accountability

- Compliance Team: Day-to-day implementation of AML protocols

- Finance Managers: Transaction monitoring and risk assessment

- Training Coordinators: Staff education and awareness

Businesses must establish robust internal mechanisms to meet their legal requirements, which involve several critical responsibilities:

- Conduct comprehensive customer due diligence

- Maintain detailed transaction records

- Implement risk assessment frameworks

- Train staff on AML procedures

- Report suspicious activities promptly

Regulatory Registration is a fundamental requirement for businesses in regulated sectors. Businesses must register with the appropriate supervisory authority, ensuring they meet all legal compliance standards.

Effective AML compliance is not just about avoiding penalties – it’s about protecting your business’s integrity and reputation.

The Senior Management’s Role encompasses:

- Developing comprehensive AML policies

- Ensuring adequate staff training

- Implementing robust monitoring systems

- Maintaining ongoing risk assessments

- Demonstrating proactive compliance commitment

Organisations must adopt a multi-layered approach to AML compliance, integrating technological solutions with human expertise to create a comprehensive defence against financial crimes.

Pro tip: Establish a dedicated compliance committee that meets regularly to review and update your AML strategies, ensuring your approach remains dynamic and responsive to changing regulatory landscapes.

Common Pitfalls And How To Avoid Them

Navigating anti-money laundering compliance requires vigilance and strategic thinking. Businesses frequently encounter critical mistakes that can compromise their regulatory standing and expose them to significant financial risks.

Common AML Compliance Mistakes include:

- Inadequate customer due diligence

- Poor record-keeping practices

- Inconsistent risk assessment

- Insufficient staff training

- Delayed suspicious activity reporting

- Neglecting ongoing transaction monitoring

Understanding these pitfalls can help organisations develop more robust compliance frameworks:

- Incomplete Customer Verification

- Inconsistent Risk Profiling

- Manual Process Limitations

- Lack of Technological Integration

- Insufficient Documentation

High-Risk Areas demand particular attention from businesses, such as:

- International transactions

- Cash-intensive businesses

- Politically exposed persons

- Complex ownership structures

- Cryptocurrency exchanges

Not all compliance failures are deliberate – many stem from genuine misunderstandings and systemic weaknesses.

Businesses must implement comprehensive strategies to mitigate these risks, including:

- Developing clear, documented AML policies

- Creating robust internal control mechanisms

- Investing in advanced compliance technologies

- Conducting regular staff training

- Establishing transparent reporting protocols

Technological solutions can significantly enhance AML compliance by providing automated monitoring, real-time risk assessment, and comprehensive reporting capabilities.

To help navigate common pitfalls, here is a summary of frequent mistakes and practical mitigation strategies:

| Compliance Mistake | Typical Consequence | Mitigation Strategy |

|---|---|---|

| Insufficient staff training | Increased human error | Ongoing training programmes |

| Delayed suspicious reporting | Regulatory fines or investigations | Automated reporting alerts |

| Manual record-keeping | Lost documentation, audit risk | Digital record management |

| Weak risk assessment | Missed suspicious activities | Regular risk profile reviews |

| Ineffective tech integration | Slow compliance response | Invest in unified platforms |

Pro tip: Conduct quarterly internal audits of your AML processes to identify potential vulnerabilities and continuously refine your compliance strategy.

Costs, Penalties, And Staying Compliant

Businesses must understand the significant financial and legal implications of anti-money laundering (AML) non-compliance. AML regulatory enforcement carries substantial risks that extend far beyond simple monetary penalties.

Potential Financial Penalties can include:

- Substantial monetary fines

- Mandatory compliance reviews

- Temporary business restrictions

- Permanent licensing revocations

- Criminal prosecution risks

The financial consequences of non-compliance are severe and multifaceted:

- Direct monetary penalties

- Legal investigation costs

- Reputational damage expenses

- Potential business interruption

- Long-term market credibility loss

Compliance Investment Breakdown:

- Training programmes

- Advanced monitoring technologies

- Compliance staff salaries

- Regular risk assessment processes

- Documentation and reporting systems

Proactive compliance is significantly more cost-effective than reactive penalty management.

Financial Conduct Authority regulations outline strict enforcement mechanisms designed to protect financial system integrity. Businesses must adopt comprehensive strategies that go beyond mere box-ticking exercises.

Successful AML compliance requires continuous investment in:

- Staff education

- Technological infrastructure

- Robust internal control mechanisms

- Regular external audits

- Adaptive risk management approaches

Pro tip: Allocate at least 2-3% of your annual compliance budget specifically for ongoing staff training and technological upgrades to stay ahead of evolving regulatory requirements.

Strengthen Your Business with Expert AML Insights and Practical Guidance

Navigating anti-money laundering checks in the UK can feel overwhelming with evolving regulations and complex compliance duties. From understanding due diligence levels to training your team and managing risks, your business deserves clear and reliable support. KefiHub offers insightful resources tailored to help UK businesses stay compliant and safeguard their reputation through practical advice and expert commentary.

Explore our comprehensive Business Archives – Kefihub for up-to-date articles that simplify your AML responsibilities and enhance your risk management strategies. Visit KefiHub today to empower your organisation with the knowledge and tools needed to meet AML regulations confidently. Don’t wait until compliance challenges become costly – start building your defence now and protect your business integrity.

Frequently Asked Questions

What are Anti-Money Laundering checks?

Anti-Money Laundering (AML) checks are legal processes that help businesses identify, prevent, and report potential money laundering risks by thoroughly examining customer transactions and identities.

Why are AML checks mandatory for businesses?

AML checks are mandatory for certain professional sectors to comply with legal requirements aimed at preventing financial crimes and ensuring the integrity of financial systems.

What is the difference between Standard Due Diligence and Enhanced Due Diligence?

Standard Due Diligence (CDD) involves basic identity verification, while Enhanced Due Diligence (EDD) includes more extensive background checks and investigations for higher-risk customers.

What are the consequences of failing to comply with AML regulations?

Failing to comply with AML regulations can result in substantial monetary fines, mandatory compliance reviews, reputational damage, and even criminal prosecution risks.

Recommended

- Why Track Business Expenses: Financial Control UK – Kefihub

- 7 Key Benefits of Registering a Business in the UK – Kefihub

- Business Registration Step by Step for UK Owners – Kefihub

- 7 Key Examples of Business Expenses for Small UK Firms – Kefihub